Introduction

The Inter-American Development Bank (IDB) is the premier development bank serving Latin America and the Caribbean (LAC) through financial assistance, technical advice, and infrastructure projects. For the last 60 years, it has provided more financing to more countries in the region for longer than any institution. For the first time in the organization’s history—and breaking with the tradition of a Latin American official leading the institution—a U.S. citizen, Mr. Mauricio Claver-Carone, assumed the presidency of the bank in October 2020. The leadership transition was contentious for some member countries and influential Democrats in the United States. The new IDB President has sought to address several organizational issues early on, including higher efficiency in operations and refocusing attention on job creation, digitalization, and nearshoring.

Most notably, Mr. Claver-Carone has suggested the need for a capital increase, a proposal which will likely be put on the table in the near future, perhaps as early as the March 2021 Annual Meeting of the IDB Board of Governors. A capital increase could enhance the IDB’s ability to support countries in the region, which were already experiencing vast development and geostrategic challenges that have now been exacerbated by the Covid-19 pandemic. A capital increase should nevertheless be regarded as one option among others to enhance the bank’s financial reach and development impact. Other avenues the bank should pursue to increase its value proposition include financial strategies such as “sweating” or stretching the capital (i.e., using its limited capital as efficiently as possible), creating special trust funds, and improving the overall operational capacity of the bank.

The capital increase option must be part of a broader discussion of the organization’s overall vision and strategic role in the LAC region for the next decade. Depending on any policy shifts that shareholders may approve alongside the capital increase, there may be potential changes to the organization’s strategic focus.

Although the bank serves the interests of the region as a whole, it is not divorced from political events impacting its member countries. A new capital increase would require political will among the shareholders and at least 75 percent approval. Since the United States owns more than 25 percent of shares (specifically, it owns 30 percent), it holds a de facto veto for capital increase and acts as a “force multiplier” for any constructive initiative within the organization. The IDB will therefore be directly affected by the political transition in the United States.

The incoming Biden administration has an ambitious agenda for the region, with a focus on Central America, the Amazon, Venezuela, and potentially the Caribbean. The first order of business for the new administration will be to consider the IDB within its Latin America strategy and decide on how to best leverage the institution as a vehicle for collective action in the region vis-à-vis other U.S. bilateral agencies (e.g., the U.S. Agency for International Development (USAID), the U.S. International Development Finance Corporation) and multilateral institutions such as the World Bank. If the Biden administration is in favor of increasing the IDB’s capital, then the key considerations it should address include the bank’s priorities for the coming decade, what role the United States should play in implementing those priorities, and how it can build support for the capital increase among a divided U.S. Congress.

A Capital Increase: What Is at Stake?

The IDB was founded in 1959 to take on some of the region’s most pressing development challenges across economic, social, institutional, and environmental sectors. In the past decade, the IDB has approved over $140 billion in loans and grants (see figure 1). The development impact is impressive: over 17 million people obtained health services through IDB programs between 2016 and 2018, and 15.7 million people benefited from targeted poverty reduction initiatives during the same period.Currently, the bank has 48 member states, 26 of which are borrowers and 22 of which are non-borrowers (see Figure 2 and Annex 1). The bank’s capital composition—the fact that a small majority of its shares has been subscribed by developing country borrowers—sets it apart from some other Multilateral Development Banks (MDBs). Unlike many other MDBs, the IDB does not have regularly scheduled reviews of capital needs. Another characteristic is that several of the borrowing members are upper middle-income countries (i.e., their income per capita is between $4,046 to $12,535) that can seek financing from capital markets instead of borrowing from the IDB. According to Moody’s rankings, 10 countries in the LAC region meet its investment grade criteria. Another four members are also members of the Organization for Cooperation on Economic Development (OECD), an organization of advanced economies.Sometime in 2021, and perhaps as early as March, the IDB’s Board of Governors may be asked to consider a potential capital increase, with significant implications for all shareholders, borrowers, and non-borrowers. This would be the tenth capital increase for the IDB. The ninth increase, IDB-9 in March 2010 (see Annex 3), was elaborated in direct response to the 2008 financial crisis; it resulted in an increase of $70 billion of total capital, of which $1.7 billion was paid-in capital and the rest was callable capital (a form of guarantee). IDB-9 was the largest capital increase in the IDB’s history, allowing the bank to lend as much as $12 billion per year and doubling the lending levels it had before the global financial crisis. Later, after the bank’s concessional window (the Fund of Special Operations) was absorbed into its Ordinary Capital in 2019, the IDB held a total equity of about $34 billion and callable capital of some $165 billion, for a combined capital of close to $200 billion.

A capital increase for the IDB would be a continuation of a trend of capital increases across the MDB system in recent years. In 2009, responding to the global financial crisis, the Asian Development Bank (ADB) increased its capital base threefold, from $55 billion to $165 billion in callable capital; in 2011, the European Bank for Reconstruction and Development (EBRD) increased its capital by 50 percent; in 2018, the World Bank approved a $7.5 billion increase in paid-in capital for the International Bank for Reconstruction and Development (IBRD); and in 2019, the African Development Bank (AfDB) increased its capital by 125 percent. The ADB case is particularly interesting, given that the increase capped shareholder contributions by 4 percent of the increased amount—minimizing the burden across parties, while greatly improving the responsiveness of the bank to need across the region. It is important to note that several of these MDBs have regularly set calendars to consider an increase (every five years, etc.). In this regard, the IDB could benefit from regularly scheduled reviews of capital needs.

Beyond Capital: Options to Enhance the Bank’s Financial Reach

The current president of the IDB has estimated that a capital increase might expand the IDB’s lending capacity from $12 billion a year to approximately $20 billion a year. However, the actual scope of the IDB’s capital constraints is not fully clear, according to an analysis from the Center for Global Development. While most agree that the IDB needs to improve its overall lending capacity, no level of financing from the IDB, or any other institution, will ever be sufficient to meet all of the region’s development needs alone, particularly since being exacerbated by the Covid-19 pandemic.

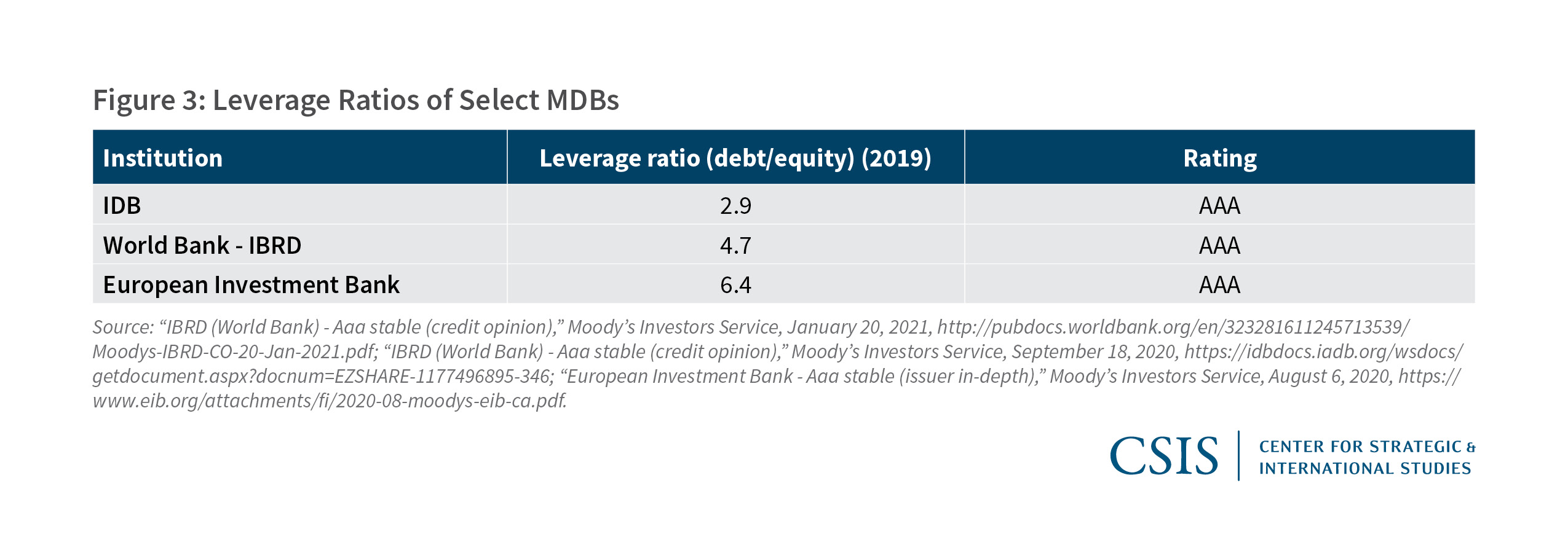

Beyond a capital increase, the bank must consider other options to enhance its financial reach, including “sweating” its capital by optimizing its balance sheet. The largest MDBs maintain AAA ratings from the major credit agencies, which permits them to borrow in the international market at inexpensive rates and lend to developing countries. To protect their AAA ratings, MDBs deploy their capital in a relatively conservative manner (Figure 3). Amongst MDBs, the IDB is among the most conservative in terms of financial leverage. While this is mostly a function of its decision-making structure, loosening capital adequacy metrics might allow for increased lending. It is not clear, however, how much headroom the IDB has for loosening its leverage ratio while still maintaining investment grade ratings. The institution would need to work with credit rating agencies to ensure that their rating processes do not provide a financial straitjacket, undermining the IDB’s ability to deliver the most financing to developing countries in the region.The IDB should also be more instrumental in channeling private capital into development projects. The IDB and its private sector arm, IDB Invest, should consider innovative ways to help catalyze additional investments through the domestic resources of developing countries (e.g., taxes, savings, and other revenues), as well as private-sector capital (e.g., equity or debt securities, real estate and other real assets, foreign direct investment (FDI), remittances, and other private sources of funding). For example, the bank could set up a first loss equity fund, maximize the use of guarantees by supporting financial intermediaries, and use blended finance tools.

The IDB could also set up project preparation facilities to assist countries with developing infrastructure projects and launch new special purpose funds inviting non-members to contribute, thereby allowing them to bid on IDB projects. Furthermore, the IDB could establish local currency funds, which would help countries mitigate foreign exchange risk and mobilize local resources from central banks in the region. As it considers a capital increase, the IDB could also establish a more permanent institutional mechanism for directing concessionary funds toward countries that are experiencing extreme fragility or crisis, such as Haiti or, eventually, Venezuela.

At the same time, the bank should pursue further operational reforms to improve its efficiency. This includes modernizing processes for staffing and resource allocation and creating more transparency regarding personnel policies. For example, the Center for Global Development found that only 55 percent of management positions were selected through competitive and transparent hiring practices. Moreover, women only represented 33 percent of the executive and representative positions. Project timelines also tend to be problematic: although there is little comparative data amongst the MDBs, according to a 2018 IDB publication “424 days elapse between a project’s approval by the Bank’s board and its first disbursement, and it takes an average of 2,040 days (5.6 years) to disburse 80 percent of the resources—ranging from a minimum of 14 days to a maximum of 4,937, depending on the project.”

The bank should seek to innovate internally, in terms of its product offerings, and be prepared to bear more risks. As it innovates, the IDB should account for changing dynamics in the region. Thinking beyond the immediate effects of Covid-19, the LAC region is home to several middle-income countries which, over time, will not need to borrow money from the IDB but can nevertheless benefit from the IDB’s deep technical expertise. While the IDB’s business model is currently predicated on lending a certain amount of money every year, a capital increase may offer a chance for the IDB to shift toward a “fee for service” approach to advisory services.

The IDB of the twenty-first century must be innovative, and yes—risk-taking.

— IDB president Mauricio Claver Carone

Crafting a Development Vision That Addresses Clear Regional Needs

A potential capital increase represents an opportunity for IDB shareholders to craft a more focused vision for the bank’s role in the region, with the goal of avoiding another lost decade. In the short term, the response to Covid-19 will be one of the IDB’s top priorities. The LAC region accounts for over a quarter of the world’s total confirmed cases of Covid-19, and the regional economy contracted by an estimated 8.1 percent during the pandemic. In response, the IDB has lent some $8 billion on immediate health response, vulnerable populations, productivity and sector employment, and fiscal management. The IDB could use additional funds to improve the region’s capacity to deploy the Covid-19 vaccine and support key economic sectors that have been hit especially hard, such as tourism and hospitality.

However, the IDB’s vision must look beyond the pandemic and address issues that have afflicted the region since long before the pandemic began. Between 2010 and 2020, originally been projected to be “the Latin American decade,” the region saw sluggish economic growth averaging at just 2.2 percent per year. The most significant period of GDP expansion occurred between 2003 and 2013, but this was fueled by a China-led commodities boom, rather than by improvements in physical and human capital or productivity. In 2021, as LAC countries recover from the pandemic, the International Monetary Fund (IMF) projects only 3.6 percent regional economic expansion, below the projected pre-pandemic trend.

Moreover, debt levels in the region have continued to rise, alongside high levels of unemployment, poverty, and inequality. These have been exacerbated by the Covid-19 pandemic. The regional unemployment rate in 2020 was 8 percent, pushing an additional 16 million people into poverty, according to the United Nations. The Center for Global Development estimates a much higher number, forecasting an additional 25 million people living in extreme poverty, alongside a 2 percent increase in the GINI coefficient, which measures inequality. With millions unemployed and earning little to no income, the pandemic has also exacerbated food insecurity in the region. National government responses to this crisis across the region have been mixed.

In November 2018, before the Covid-19 pandemic, CSIS’s Dan Runde and Juan José Daboub had recommended the following five new priority areas for IDB: private sector development, inclusive growth, quality infrastructure, governance and the fight against corruption, regional security and stability, and productivity and innovation. These issue areas should continue to be of interest to the IDB, as they have now been exacerbated by the onset of the pandemic. Today, additional capital funds might be used to build out digital infrastructure, support education and training to enable the future of work in the region, address climate challenges including adaptation, build new energy grid systems, support a second Caribbean Basin Initiative, or promote cooperative action to confront corruption and money laundering.

As the IDB Group presents its strategic vision for the region, it should continue to develop its autonomous private sector innovation lab, which was previously known as the Multilateral Investment Fund but was recently rebranded as IDB Lab. IDB Lab has mobilized over $2 billion in the form of impact investment and blended financing since it was first founded in 1993. Its projects focus primarily on identifying and supporting private-sector solutions to the development challenges that have traditionally afflicted the LAC region, with a focus on high-impact enterprises that help poor and vulnerable populations. The Lab is also an “innovation broker,” meaning that it curates and disseminates knowledge on topics ranging from blockchain regulation to agricultural technology to the “silver economy.” The Lab is financed by a Committee of Donors, the largest of which have historically been the United States and now Japan. Beginning in 2023, however, IDB Lab will need to seek out alternative sources of funding at the request of the Committee of Donors.

An Opportunity to Expand Membership?

In addition to taking on new sector priorities, a potential capital increase also offers an opportunity to reset the relationship between IDB’s shareholders, non-borrowers, and borrowers, including discussions on the composition of these groups. Until now, the region’s borrowers have been unwilling to have their slight majority diluted by new shareholders.

The IDB could be an appropriate vehicle by which to respond to competing economic and geopolitical interests in the region, particularly related to China. While China only holds 0.004 percent of IDB shares, it is the largest trading partner of several countries in the region, many of which have joined the Belt and Road Initiative and the Asia Infrastructure Investment Bank. As such, China would likely seek to expand its shareholding in the IDB if given the option. By issuing more shares, the IDB could, alternatively, bring in Australia, India, or Qatar as new shareholders of the IDB or IDB Invest. Taiwan, which is recognized by nine countries in the Western Hemisphere, could also join as an “economy,” like its membership in the ADB.

In seeking new members, the IDB may look to its Trust Fund partners. Australia, for example, has an $8.8 million Partnership Trust Fund for Poverty Reduction in Latin America. Established in 2011, this trust fund supports access to financial services, access to markets and capabilities for youth employment, and access to basic services. The trust fund provides grants for financial services, skills training, effective farming technologies, and basic services.

India, while not a Trust Fund partner, has established limited cooperation with the bank, starting with a trip by the former president of the IDB to India in 2010 for consultations on India’s role in Latin America. Subsequent analysis by the bank in 2018 identified that trade between India and the region had reached $30 billion, with potential for growth in the coming decade. The region is also home to some 200 Indian companies employing over 50,000 local workers, suggesting that many of the ties necessary for India to take on shareholder status are in place.

Conversations about new shareholders should be accompanied by the possibility of graduating countries from borrower status. This is especially relevant for Chile, Colombia, Costa Rica, and Mexico—all of which are OECD members with investment grade that can seek financing from capital markets. Graduation would be difficult to achieve, especially considering that these upper middle-income countries are critical to the IDB’s financial stability and risk distribution. The EBRD, for example, has only done it once, while the IBRD has graduated 25 countries since it was founded in 1944.

Otherwise, the IDB’s work with these upper middle-income countries should continue to serve as an opportunity for the Bank to improve program design, with the aim of applying those lessons to projects on other countries. The conversation about “rightsizing” membership can also offer opportunities for reform and reflection. It is important to consider what the role of the IDB is for countries that can access capital elsewhere, as well as what type of reforms can be put in place to support that relationship. Raising that question pushes the IDB to consider its value add (its “additionality”) for projects and loans in upper middle-income countries beyond the provision of capital itself. The process of reflecting on these benefits offers shareholders an opportunity to engage with the bank in novel ways. Answers could include knowledge, technical expertise (free or reimbursed), network benefits, or credibility, among others.

Is It Time for a Capital Increase for IDB Invest Too?

The conversation regarding a capital increase for the IDB will also raise questions as to whether IDB Invest, the private sector arm of the IDB, should get its own capital increase. IDB Invest is a separate legal entity with its own board of directors chaired by the president of the IDB. Its ownership structure is distinct from that of the Bank; the United States holds just 13.35 percent of shares of IDB Invest. IDB Invest has become an increasingly important member of the IDB Group—with a portfolio of $12.1 billion—as the Group expands its focus on the private sector.

There is a variety of views about IDB Invest. Some see the money for IDB Invest as a “zero sum game,” meaning that the monies going to IDB Invest are being “taken away” from other activities focused on the public sector. The thinking among these shareholders may reflect outdated views or views out of step with the global zeitgeist on the role of the private sector in development. It also perhaps misses the fact that most monies paying for basic human needs and public services come from taxes paid for by the formal private sector, so growing the formal private sector means jobs and money for public service and basic human needs.

Though IDB Invest is a valuable component of the IDB Group, member countries may be more reluctant to give a capital increase to IDB Invest, which does not have callable capital. There has also been significant effort over the past few years to separate IDB Invest from the Bank, and this division should remain clear throughout the capital increase process. IDB Invest could get an increase if members are willing to open up some Invest shares to other countries, which could be asked to contribute to trust funds as part of their membership terms. With this additional capital, IDB Invest could continue to be the key vehicle by which the IDB Group repositions itself as a lender of choice for Latin American businesses in a wide range of sectors, including manufacturing, sanitation, agriculture, telecommunications, finance, and tourism. One option would be to consider a capital increase for both institutions together, as the World Bank did in 2018 with the IBRD and the International Finance Corporation (IFC). Doing so might require IDB Invest to strengthen its development effectiveness focus, address clearly identified market failures that hinder the private sector in the region, and avoid displacing or competing with private sector financial operators.

What Are U.S. Interests in a Potential Capital Increase?

A potential capital increase also offers the United States an opportunity to leverage its interests within the organization, both in terms of operational priorities as well as in terms of development thrusts. In its most basic form, the United States will need to decide whether it should fund the capital increase. The estimated amount for the capital increase is still unclear, but if shareholders are required to invest a similar amount as they were in the 2010 increase, this would amount to approximately $2 billion in paid-in capital. As a 30 percent shareholder, the United States would have to contribute an estimated total of $600 million. As with the 2010 increase, the United States could pay in installments over a period of five years, allowing it to manage the investment against other competing priorities. Although a large sum, this would amount to $120 million a year for 5 years, which is manageable within the overall U.S. foreign aid budget of $35 billion annually.

Despite these significant outlays, the net cost of the IDB to the U.S. Treasury is close to zero. This is in large part since the IDB is headquartered in the Washington, D.C., meaning that a large proportion of its employees—including 750 U.S. citizens—and contractors are based in the United States and pay U.S. income taxes. The IDB also maintains significant engagements with U.S. companies for consulting, legal, and other services, which ultimately also contribute to the Treasury in the form of taxes. Taking these factors into account, the IDB has actually brought more money into the U.S. Treasury over the last 15 years than it has received.

To finance the capital increase, the U.S. Congress would need to appropriate funds to the foreign aid budget (i.e., the international affairs account, known as the “150 account”). Under the new Biden administration, the U.S. Congress is likely to receive significant requests for an increase in the 150 account for other purposes, which is expected to include $4 billion for the LAC region’s development to be divided between USAID, the State Department, and other U.S. agencies. Within the region, the Biden administration will likely be interested in expanding aid to Central America through a revamped Alliance for Prosperity 2.0 led by the Northern Triangle countries. Moreover, Democrats in the U.S. Congress may be unwilling to support an IDB capital increase under the leadership of the current IDB president, whose candidacy drew criticism from top Democratic senators and spokespeople from Biden’s presidential campaign.

As mentioned earlier, U.S. policymakers will need to weigh the value of maintaining the country’s 30 percent shareholding against diluting its position within the institution. If the United States does not maintain its capital position, this offers opportunities for other shareholders to increase their stakes. Any dilution of U.S. shares could be supplanted by new shareholders (like Taiwan), but it also risks current shareholders (like China) consolidating their influence. U.S. policymakers should consider the ideal shareholder status that allows the United States to retain de facto veto power while also bringing in new shareholders.

The United States can also push for a more systemic review of capital needs across the different MDBs. These institutions have gone back to their shareholders on repeated occasions to expand their capital basis. A more thorough and systematic review of each institution’s strengths, weaknesses, and division of labor within the international system would be a more effective way for shareholders to make decisions on capital allocations going forward. This may result in a standardization across capital increase discussions or a common timeline for potentially assessing capital needs. The World Bank and the IDB could host joint Board of Governors meetings every three years, and they could align their strategic planning cycles. However, the fact that shareholders and their participations vary across institutions—and that they may have different views and interests—will have to be taken into consideration when analyzing standardized practices.

In addition to the resetting the landscape of shareholders and borrowers, a capital increase negotiation could offer a unique opening for the United States to advance the development priorities of the Biden administration. In the first place, the United States should pursue accelerated growth and overall financial stability in the region, supporting the work of the IDB and the IMF to restart economic growth and manage debt levels—especially considering the devastating social, health, and economic effects of the Covid-19 pandemic. Regional growth rates have fallen below the international average of 4.1 percent, with debt levels continuing to rise since 2008, constituting 47.2 percent of regional GDP.

With additional capital, the IDB may improve the region’s economies by supporting a stronger regulatory environment, promoting efficient trade policies and practices, and improving coordination and shared advocacy in international trade negotiations. Furthermore, it could help countries in the region establish economic zones, modernize infrastructure for trade, develop regional energy systems that support improved trade, and support small and medium business that need help accessing the larger production chain. The capital increase would also support nearshoring, which would benefit the U.S. economy through its close links to the LAC region.

Special attention should be given to Central America, a geostrategic region for the United States. During the ninth capital increase, in 2010, a new financial support package was devised for Haiti, resulting in mandated debt relief of $447 million and new grant financing of $2.2 billion over a ten-year period (see annex 2). The lessons from Haiti during the IDB’s ninth increase deserve additional analysis in the lead up to a potential tenth increase. A similar package can be put forward for the poorest countries of Central America (i.e., the Northern Triangle countries of Guatemala, El Salvador, and Honduras) and the Caribbean in exchange for major policy reforms on the part of those governments. The United States can support projects that improve citizen security in the Northern Triangle and address the underlying root causes of migration. During 2019, an unprecedented 608,000 unauthorized migrants from the Northern Triangle, over 80 percent of whom were unaccompanied minors, were apprehended at U.S. border.

The necessary interventions involve a mix of economic, development, political, and security reforms. Controversial anti-crime policies in the region have significantly expanded police powers and enacted harsher punishments for gang members. However, corruption is rampant, and transnational criminal organizations have consolidated power, leaving people with little trust in law enforcement agencies and other security institutions. The initial Alliance for Prosperity (A4P) program for this region (managed by the IDB), yielded results for the period of 2017–2018, notably in the economic sector. However, it is not clear how much of the A4P funding was additive versus repurposing of existing funding. A potential capital increase might build on these outcomes to improve trust in these systems and make meaningful progress on the underlying root causes of violence and migration.

Addressing citizen security may also consist of components to empower youth and improve educational attainment in the region. Youth make up 20 percent of the region’s population, but the unemployment rate for the 15–29 age group is three times as high as it is for the population between 30–64 years of age. Deaths by violent acts and homicides in the 15–24 age group accounted for 43 percent of the total mortality rate, and young men are especially vulnerable. A potential capital increase might go toward improving youth access to education, bringing the private sector into the education system, building resilience of national education systems, and improving quality educational infrastructure (including online learning). The cumulative impact will amount to improved levels of human capacity through access to higher quality education and vocational training. Additional programming, improved health care access, social protection systems for the most vulnerable will further improve the region’s stability.

Another area where the United States could leverage its position in the IDB is to counteract regional dependency on China, which has been using predatory economic practices, aggressive messaging, and diplomatic outreach—alongside its Belt and Road transactions—to expand its influence in the region. China has also driven several LAC countries away from recognizing Taiwan—and from the expanded commercial opportunities for Taiwan’s companies and markets for its exports in the LAC region—through practices that undermine national sovereignty. For example, the IDB may be well-positioned to help the region develop and deploy communications technology without becoming overly dependent on China.

The region faces several barriers to developing and deploying new technologies, including issues related to financing, pricing, limited land size, and lack of radio frequencies. Amid the economic effects of Covid-19, the region has also been unable to invest more robustly in 5G spectrum technology. These barriers have opened a gap in telecommunications infrastructure now being filled by Chinese Huawei, signaling a potential increase in surveillance and censorship. With new funding, the IDB could potentially provide technical support, targeted outreach about the danger of such partnerships, specific support to online learning and health planforms, improvement in cybersecurity systems, digital payment systems, monitoring, and strategic planning on the transition to 5G.

Finally, a decade of opportunity would also include the possibility of Cuba and Venezuela opening up toward democratic systems and free market economies. Whenever Venezuela achieves an end to its political crisis, the country will be a ward of the international development system for years. It will require continuous assistance from MDBs to rebuild infrastructure, address acute humanitarian needs, and recover its private sector. This is a robust undertaking. The United States and the IDB are poised to play a critical role in this transition effort, not just in the form of loans but also through technical assistance to ensure good governance, a resilient private sector, and sound fiscal management.

Conclusion: The Way Forward

The IDB is a critical institution not only in terms of financing and technical advice, but as a vehicle for collective action for the region. A capital increase is one of few ways that the United States and other shareholders can make significant shifts in the future direction of the IDB. Deciding whether to move forward with a potential increase will require U.S. policymakers and the U.S. Congress to examine current priorities against the realities of the region and to consider the IDB’s relatively minimal impact on the Treasury. Short of a capital increase, the bank should consider ways to increase its leverage, use its capital more efficiently, and work more seamlessly in concert with the rest of the MDB system, international organizations, and bilateral aid agencies.

There is no doubt that the LAC region needs more financial assistance. Covid-19 has had a detrimental impact on the region’s economy, pushing millions into poverty and food insecurity, and the pandemic is putting private businesses in precarious situations. The IDB and IDB Invest are positioned to assist in the region’s post Covid-19 recovery and to tackle issues that affect the entire region, such as climate change and intra-regional trade. The additional capital could also be used to help address the root causes of migration from Northern Triangle, and, eventually, stabilize and rebuild Venezuela.

The capital increase also represents a rare opportunity to review and revise key aspects of the bank’s ownership, operations, and management, to improve its technical capacity, and to push it to work more efficiently in concert with the rest of the MDB system. Shares could be diluted—either in the IDB, IDB Invest, or both— to bring in additional economies with significant influence in Latin America, such as India and Taiwan, providing a necessary counterweight to China’s growing influence in the region.

Ultimately, it will be up to the shareholders to develop and articulate a coherent vision for the IDB’s future role in the region.

Originally published on csis.org.

{kind=link}

{kind=link}

{kind=link}

Leave a comment